In Spring 2022, EUROCROWD conducted a questionnaire on VAT on crowdfunding platforms. Given an ongoing court case in an EU member state against a crowdfunding platform regarding their treatment of VAT, we wanted to look for input into how other platforms across the EU deal with this issue. Taxation remains national and treatment of crowdfunding activities and returns may vary from country to country.

During our Mastering ECSP webinar series, also this spring, we took a closer look at this topic including tax treatment for project owners, platforms and investors together with Dr. Mathias Link, tax partner at PwC in Frankfurt. In the case of Germany services connected to financial assets or financial services are VAT relevant. While VAT generally applies, certain services are, however, VAT exempt. These services include intermediation services in respect of granting a loan or the assignment of a claim. The German tax authorities have taken the view that crowdfunding platforms are treated as fully VAT exempt because the main purpose of the platform is to bring together investors and project owners.

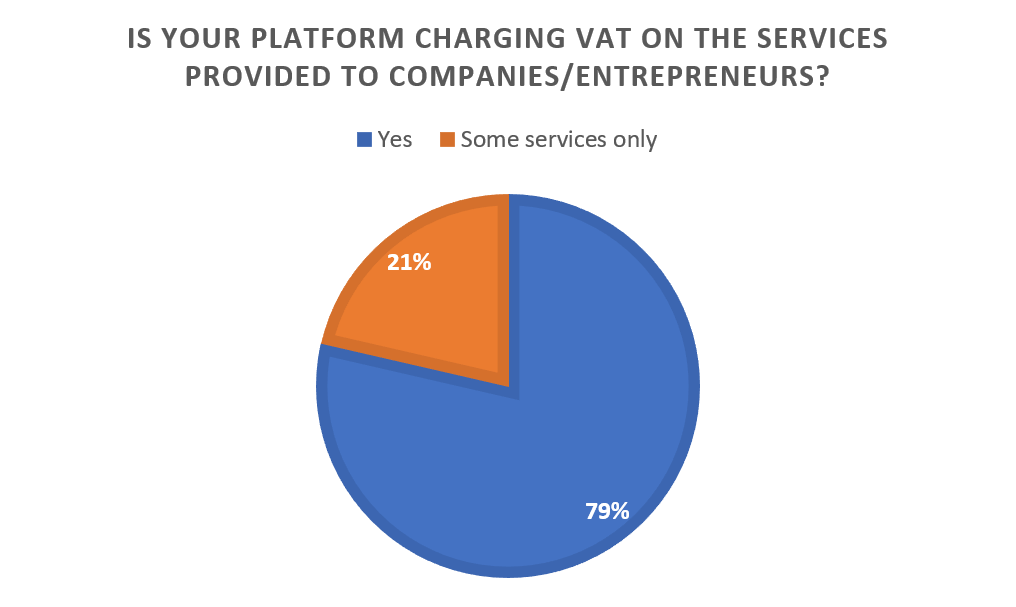

Nonetheless, the results of our questionnaire show that almost 80% of the participating crowdfunding platforms are actually charging VAT on the services provided to companies or entrepreneurs; and 21% charge VAT partially, only to some services, see the graph below.

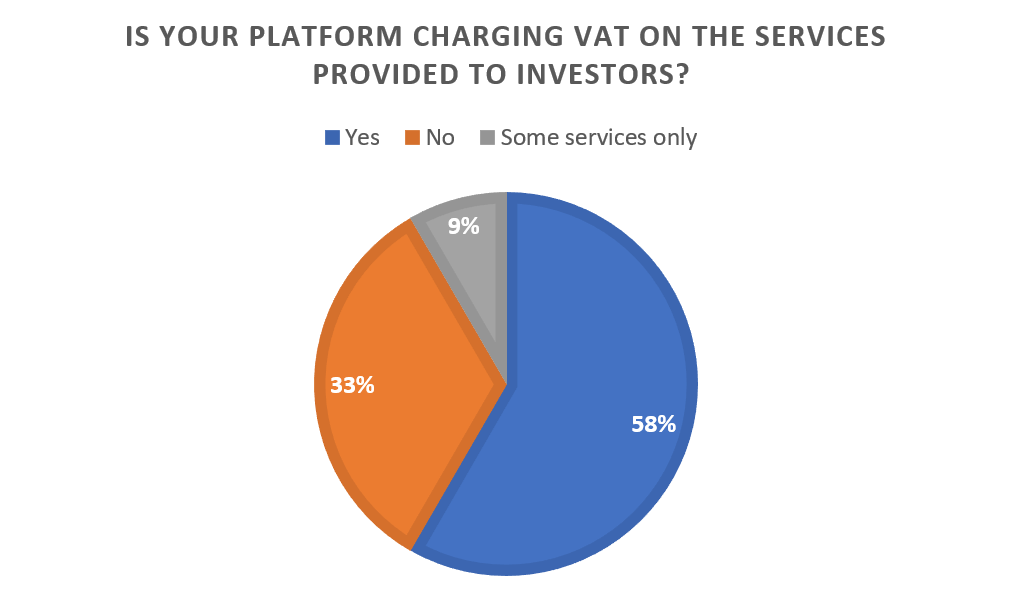

In the case of services provided to investors, more than half of the platforms are charging VAT, 33% state that they do not charge VAT and 9% of the platforms charge VAT only to some services (see the graph).

With ECSP in force, we can expect that tax matters for crowdfunding campaigns become even more relevant due to the increased number of cross-border offerings. ECSP core services are expected to be also treated as intermediation services and therefore VAT exempt. Unclear is how additional services might be treated. Here it will likely depend on the types of services a platform offers and if they can be seen as a whole with the intermediation service. National Tax authorities will have to provide clarification on this in due course.

Thank you to all the participants for taking the time to complete the questionnaire. EUROCROWD will revisit the topic of taxation under ECSPR on the 8 November 2022, on the first day of our forthcoming 11th CrowdCon: Next Level – Expanding the Capital Markets Union.